The Greatness Machine is on a Quest to Maximize the Human Experience! Join Award Winning CEO and Author, Darius Mirshahzadeh (pron. Mer-shaw-za-day), as he interviews some of the greatest minds in the world―turning their wisdom and experience into learnings and advice you can use in your life so that you can level up and create greatness. Join Darius as he goes deep with guests like: Moby, Seth Godin, Gabby Reece, Amanda Knox, UFC Ring Announcer Bruce Buffer, Former FBI Negotiator Chris Voss ...

…

continue reading

Not Your Average Financial Podcast™에서 제공하는 콘텐츠입니다. 에피소드, 그래픽, 팟캐스트 설명을 포함한 모든 팟캐스트 콘텐츠는 Not Your Average Financial Podcast™ 또는 해당 팟캐스트 플랫폼 파트너가 직접 업로드하고 제공합니다. 누군가가 귀하의 허락 없이 귀하의 저작물을 사용하고 있다고 생각되는 경우 여기에 설명된 절차를 따르실 수 있습니다 https://ko.player.fm/legal.

Not Your Average Financial Podcast™와 비슷한 콘텐츠

Custom Manufacturing Industry podcast is an entrepreneurship and motivational podcast on all platforms, hosted by Aaron Clippinger. Being CEO of multiple companies including the signage industry and the software industry, Aaron has over 20 years of consulting and business management. His software has grown internationally and with over a billion dollars annually going through the software. Using his Accounting degree, Aaron will be talking about his organizational ways to get things done. Hi ...

…

continue reading

How can business help solve society’s biggest challenges? Welcome to Series 3 of Take on Tomorrow, the award-winning podcast from PwC that examines the biggest problems facing society and the role business can—and should—play in solving them. This series, we’re welcoming broadcaster and journalist Femi Oke to the show. She joins podcaster and journalist Lizzie O’Leary, and together with industry innovators, tech trailblazers and visionary leaders from around the globe, they’ll explore timely ...

…

continue reading

Montgomery & Co. is a weekly podcast where WNBA champion and part-owner of the Atlanta Dream Renee Montgomery is joined by her mother Bertela Montgomery, her sister Nicole Young and her wife Sirena Grace as they chart a unique path through the business world as four black and brown women keeping their family first at all times. Both insightful and compelling, this one-of-a-kind talk show combines interviews with some of the world’s top innovators & entrepreneurs with sports and culture conve ...

…

continue reading

Wharton faculty and industry leaders discuss their latest research, books, and relevant business topics. Hosted on Acast. See acast.com/privacy for more information.

…

continue reading

Alessandro Bogliari, CEO and Co-Founder of The Influencer Marketing Factory, a global influencer marketing agency, talks with great guests about influencer marketing, social media, the creator economy, social commerce and much more.

…

continue reading

The day's biggest news dissected by the day's newsmakers. Diverse opinions from across the political spectrum. The show that makes you decide, are you the Left, Right or the Centre?

…

continue reading

A unicorn is a magical creature shrouded in mystery known for its ability to make the impossible possible. In modern times, the word “unicorn” has come to mean something intrinsically valuable and difficult to obtain, whether that be a business with a $1 billion dollar valuation, or the love of a special someone. On Zero to Unicorn, we’ll hear directly from the Kaeding family as they recount their history of founding and operating Norhart, a unicorn-level business in the construction industr ...

…

continue reading

It didn’t all change in March 2020. Not really. The UK high street has been in the throes of a gradual revolution for decades. From the rise of ecommerce, to the birth of mobile, social commerce, and a growing emphasis on experience, change has been underway for a while. In fact for many, the pandemic has acted as a wake-up call. Digital transformation was no longer a ‘nice to have’ but a matter of survival. Necessity sparked innovation and customers are enjoying more flexibility and conveni ...

…

continue reading

Best Business Podcast (Gold), British Podcast Awards 2023 How do you build a fully electric motorcycle with no compromises on performance? How can we truly experience what the virtual world feels like? What does it take to design the first commercially available flying car? And how do you build a lightsaber? These are some of the questions this podcast answers as we share the moments where digital transforms physical, and meet the brilliant minds behind some of the most innovative products a ...

…

continue reading

Player FM -팟 캐스트 앱

Player FM 앱으로 오프라인으로 전환하세요!

Player FM 앱으로 오프라인으로 전환하세요!

))

Episode 345: Direct vs. Non-Direct Policy Loans, The Debate and The Truth

Manage episode 412079541 series 1610796

Not Your Average Financial Podcast™에서 제공하는 콘텐츠입니다. 에피소드, 그래픽, 팟캐스트 설명을 포함한 모든 팟캐스트 콘텐츠는 Not Your Average Financial Podcast™ 또는 해당 팟캐스트 플랫폼 파트너가 직접 업로드하고 제공합니다. 누군가가 귀하의 허락 없이 귀하의 저작물을 사용하고 있다고 생각되는 경우 여기에 설명된 절차를 따르실 수 있습니다 https://ko.player.fm/legal.

In this episode, we ask:

- What is a policy loan?

- Why do we love the Bank on Yourself® type whole life insurance policies?

- Is a non-direct recognition policy loan the best feature in the financial universe?

- What is a direct recognition policy loan?

- Is there really no difference between the two?

- Does it really matter?

- Why is transparency key?

- What is the history between non-direct recognition and direct recognition policy loans?

- How long have life insurance policies loans been around?

- Over 150 years ago, how did insurers treat these separate loans with distinct interest rates?

- What about collateral?

- What about the life insurance general fund?

- What about using your policy as collateral?

- What about dividends?

- How would the policy continue to earn interest?

- Where is the money for the loan coming from exactly?

- Why did some insurance companies move over to do direct recognition policy loans?

- Why did some insurance companies hold firm with non-direct recognition policy loans?

- What is a mutual life insurance company?

- What about profits?

- Who should logically have a higher dividend?

- Who is penalized?

- Do companies offering direct recognition policy loans offer slightly higher dividends?

- Who is going to have a better experience?

- What good is that cash value if you can’t collateralize it?

- What about the living benefits of life insurance?

- What is outrageous?

- What did Nelson Nash say?

- Who has real liquidity?

- What about direct recognition policy loans for a time horizon (for 10 years, etc.)?

- How about an example?

- What is a 1035 exchange (a like-kind exchange for life insurance)

- Would you like to learn more in Episode 252?

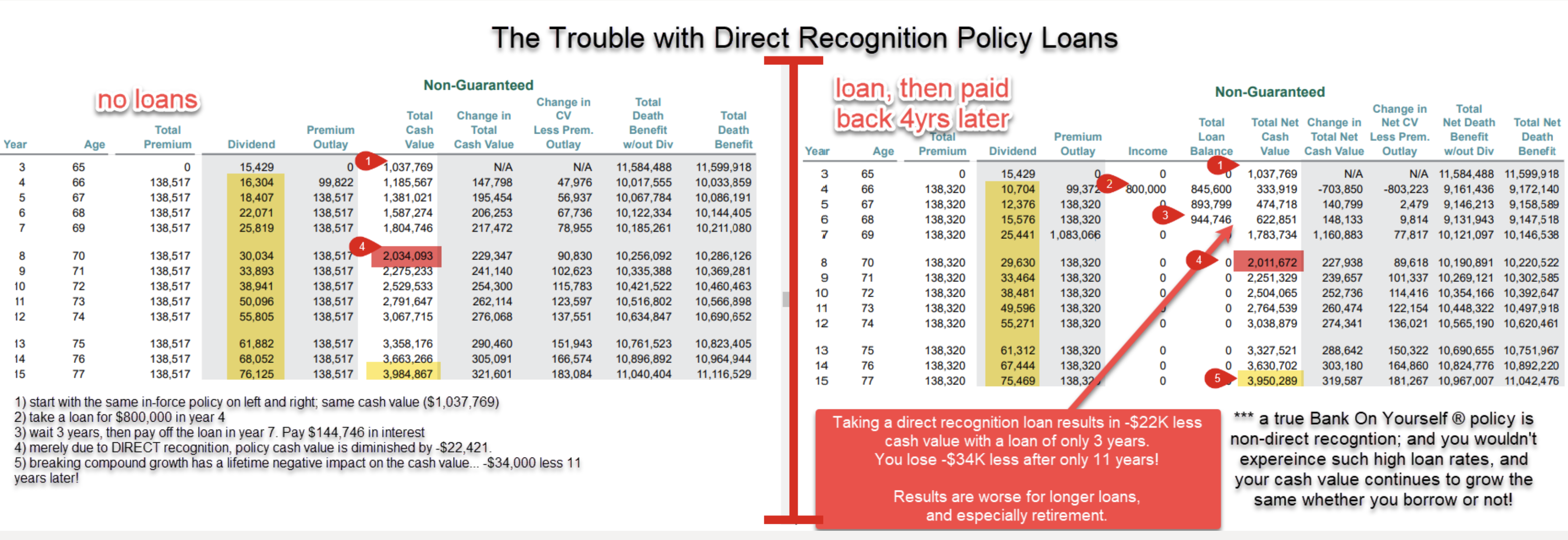

- What happens in a scenario where direct recognition policy loans were taken?

- What happens in a scenario where non-direct recognition policy loans (as in a Bank on Yourself type whole life insurance policy) were taken?

- What about the dollar diagram?

- What about the one dollar?

- What happens if you put this single dollar into a paid up additions rider (PUAR)?

- What about opportunity cost?

- What happens if you spend that dollar instead of saving it?

- What is the interest?

- What benefits you?

- What about dividends?

- How do the insurers earn money for dividends?

- How does that benefit policy holders?

- How much would you have?

- How many dollars…?

- Is there such a thing as paying too much premium?

- How about another example about a policy loan to purchase a car?

- What did the three cars cost you?

- How much did you net in the non-direct recognition policy loan’s policy?

- Knowing all of this, why would you buy a car any other way?

- Should you just get a bank loan?

- What totally defeats the purpose of Bank on Yourself®?

- Are you being penalized?

- Which scenario keeps me more in control of my own money?

- Which scenario yields control to the bank?

- What about Bank on Yourself® policy engineering?

- Would you like to meet with Mark?

- Would you join us next week?

The topics and images presented in this podcast are general information only and not for the purposes of providing legal, accounting or investment advice. On such matters, please consult a professional who knows your specific situation.

332 에피소드

Manage episode 412079541 series 1610796

Not Your Average Financial Podcast™에서 제공하는 콘텐츠입니다. 에피소드, 그래픽, 팟캐스트 설명을 포함한 모든 팟캐스트 콘텐츠는 Not Your Average Financial Podcast™ 또는 해당 팟캐스트 플랫폼 파트너가 직접 업로드하고 제공합니다. 누군가가 귀하의 허락 없이 귀하의 저작물을 사용하고 있다고 생각되는 경우 여기에 설명된 절차를 따르실 수 있습니다 https://ko.player.fm/legal.

In this episode, we ask:

- What is a policy loan?

- Why do we love the Bank on Yourself® type whole life insurance policies?

- Is a non-direct recognition policy loan the best feature in the financial universe?

- What is a direct recognition policy loan?

- Is there really no difference between the two?

- Does it really matter?

- Why is transparency key?

- What is the history between non-direct recognition and direct recognition policy loans?

- How long have life insurance policies loans been around?

- Over 150 years ago, how did insurers treat these separate loans with distinct interest rates?

- What about collateral?

- What about the life insurance general fund?

- What about using your policy as collateral?

- What about dividends?

- How would the policy continue to earn interest?

- Where is the money for the loan coming from exactly?

- Why did some insurance companies move over to do direct recognition policy loans?

- Why did some insurance companies hold firm with non-direct recognition policy loans?

- What is a mutual life insurance company?

- What about profits?

- Who should logically have a higher dividend?

- Who is penalized?

- Do companies offering direct recognition policy loans offer slightly higher dividends?

- Who is going to have a better experience?

- What good is that cash value if you can’t collateralize it?

- What about the living benefits of life insurance?

- What is outrageous?

- What did Nelson Nash say?

- Who has real liquidity?

- What about direct recognition policy loans for a time horizon (for 10 years, etc.)?

- How about an example?

- What is a 1035 exchange (a like-kind exchange for life insurance)

- Would you like to learn more in Episode 252?

- What happens in a scenario where direct recognition policy loans were taken?

- What happens in a scenario where non-direct recognition policy loans (as in a Bank on Yourself type whole life insurance policy) were taken?

- What about the dollar diagram?

- What about the one dollar?

- What happens if you put this single dollar into a paid up additions rider (PUAR)?

- What about opportunity cost?

- What happens if you spend that dollar instead of saving it?

- What is the interest?

- What benefits you?

- What about dividends?

- How do the insurers earn money for dividends?

- How does that benefit policy holders?

- How much would you have?

- How many dollars…?

- Is there such a thing as paying too much premium?

- How about another example about a policy loan to purchase a car?

- What did the three cars cost you?

- How much did you net in the non-direct recognition policy loan’s policy?

- Knowing all of this, why would you buy a car any other way?

- Should you just get a bank loan?

- What totally defeats the purpose of Bank on Yourself®?

- Are you being penalized?

- Which scenario keeps me more in control of my own money?

- Which scenario yields control to the bank?

- What about Bank on Yourself® policy engineering?

- Would you like to meet with Mark?

- Would you join us next week?

The topics and images presented in this podcast are general information only and not for the purposes of providing legal, accounting or investment advice. On such matters, please consult a professional who knows your specific situation.

332 에피소드

모든 에피소드

×플레이어 FM에 오신것을 환영합니다!

플레이어 FM은 웹에서 고품질 팟캐스트를 검색하여 지금 바로 즐길 수 있도록 합니다. 최고의 팟캐스트 앱이며 Android, iPhone 및 웹에서도 작동합니다. 장치 간 구독 동기화를 위해 가입하세요.

Not Your Average Financial Podcast™와 비슷한 콘텐츠

The Greatness Machine is on a Quest to Maximize the Human Experience! Join Award Winning CEO and Author, Darius Mirshahzadeh (pron. Mer-shaw-za-day), as he interviews some of the greatest minds in the world―turning their wisdom and experience into learnings and advice you can use in your life so that you can level up and create greatness. Join Darius as he goes deep with guests like: Moby, Seth Godin, Gabby Reece, Amanda Knox, UFC Ring Announcer Bruce Buffer, Former FBI Negotiator Chris Voss ...

…

continue reading

Custom Manufacturing Industry podcast is an entrepreneurship and motivational podcast on all platforms, hosted by Aaron Clippinger. Being CEO of multiple companies including the signage industry and the software industry, Aaron has over 20 years of consulting and business management. His software has grown internationally and with over a billion dollars annually going through the software. Using his Accounting degree, Aaron will be talking about his organizational ways to get things done. Hi ...

…

continue reading

How can business help solve society’s biggest challenges? Welcome to Series 3 of Take on Tomorrow, the award-winning podcast from PwC that examines the biggest problems facing society and the role business can—and should—play in solving them. This series, we’re welcoming broadcaster and journalist Femi Oke to the show. She joins podcaster and journalist Lizzie O’Leary, and together with industry innovators, tech trailblazers and visionary leaders from around the globe, they’ll explore timely ...

…

continue reading

Montgomery & Co. is a weekly podcast where WNBA champion and part-owner of the Atlanta Dream Renee Montgomery is joined by her mother Bertela Montgomery, her sister Nicole Young and her wife Sirena Grace as they chart a unique path through the business world as four black and brown women keeping their family first at all times. Both insightful and compelling, this one-of-a-kind talk show combines interviews with some of the world’s top innovators & entrepreneurs with sports and culture conve ...

…

continue reading

Wharton faculty and industry leaders discuss their latest research, books, and relevant business topics. Hosted on Acast. See acast.com/privacy for more information.

…

continue reading

Alessandro Bogliari, CEO and Co-Founder of The Influencer Marketing Factory, a global influencer marketing agency, talks with great guests about influencer marketing, social media, the creator economy, social commerce and much more.

…

continue reading

The day's biggest news dissected by the day's newsmakers. Diverse opinions from across the political spectrum. The show that makes you decide, are you the Left, Right or the Centre?

…

continue reading

A unicorn is a magical creature shrouded in mystery known for its ability to make the impossible possible. In modern times, the word “unicorn” has come to mean something intrinsically valuable and difficult to obtain, whether that be a business with a $1 billion dollar valuation, or the love of a special someone. On Zero to Unicorn, we’ll hear directly from the Kaeding family as they recount their history of founding and operating Norhart, a unicorn-level business in the construction industr ...

…

continue reading

It didn’t all change in March 2020. Not really. The UK high street has been in the throes of a gradual revolution for decades. From the rise of ecommerce, to the birth of mobile, social commerce, and a growing emphasis on experience, change has been underway for a while. In fact for many, the pandemic has acted as a wake-up call. Digital transformation was no longer a ‘nice to have’ but a matter of survival. Necessity sparked innovation and customers are enjoying more flexibility and conveni ...

…

continue reading

Best Business Podcast (Gold), British Podcast Awards 2023 How do you build a fully electric motorcycle with no compromises on performance? How can we truly experience what the virtual world feels like? What does it take to design the first commercially available flying car? And how do you build a lightsaber? These are some of the questions this podcast answers as we share the moments where digital transforms physical, and meet the brilliant minds behind some of the most innovative products a ...

…

continue reading

Player FM -팟 캐스트 앱

Player FM 앱으로 오프라인으로 전환하세요!

Player FM 앱으로 오프라인으로 전환하세요!